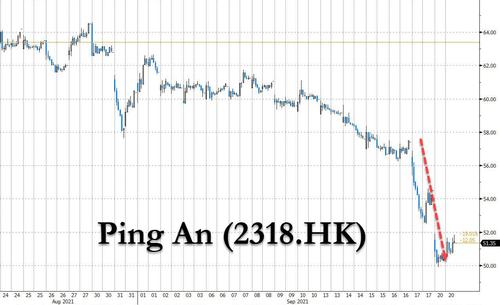

Few were surprised to see that the crash in Evergrande dragged down property names (one among then, Sinic Holdings), crashed 87% in minutes and was halted), banks exposed to the property developer (according to report there are over 120), with the contagion spreading to commodities directly linked to China's property sector (such as Iron Ore which plunged 10%), as well as FX of commodity-heavy countries, one ominous decline was that of Asia Pacific's largest insurer, Ping An (whose name literally and unironically means "safe and well"), which dropped 3%, following a 5% drop on Friday, and hitting a four year low on concerns about its property exposure.

The selling took place even though the company issued a statement Friday saying that its insurance funds have "zero exposure" to Evergrande and other real estate companies "that the market has been paying attention to." Real estate accounts for about 4.9% of Ping An Insurance's investments, versus an average 3.2% for peers, according to Bloomberg Intelligence.

"For real estate enterprises that the market has been paying attention to, PA insurance funds have zero exposure, neither equity or debt, including China Evergrande," Ping An said in a statement as it rushed to reassure investors.

While it may have no exposure, Ping An does have RMB63.1bn or $9.8bn in exposure to Chinese real estate stocks across its RMB3.8TN ($590BN) of insurance funds, and took a $3.2BN hit in the first half of the year after the default of another developer, China Fortune Land Development. The insurer is also head of the creditor committee for China Fortune Land, which specialises in industrial parks in Hebei province and suffered from delayed local government payments. One of its restructuring advisers, Admiralty Harbour Capital, was hired by Evergrande this week.

At a time when any Evergrande counterparties or even rumored counterparties are immediately deemed radioactive, Ping An's plight demonstrates how acute and widespread the selloff could become in China if Beijing fails to intervene.

"I expect a lot of financial institutions could be hit by the worries" about Evergrande, said Zhou Chuanyi, a Singapore-based analyst at Lucror Analytics. "As long as a financial institution has exposure to developers, Evergrande should take quite a significant share of that."

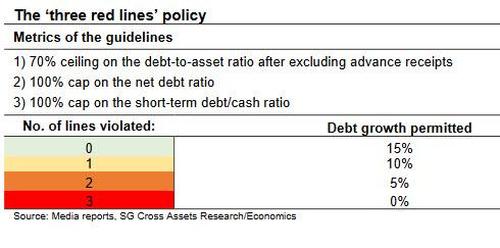

Yet as the market waits for some response official response, hopeful that Beijing will step in, we discussed earlier that China's policymakers have instead sought to crack down on excessive leverage across its vast real estate sector over the past years, which makes up more than a quarter of the economy, imposing a firm threshold known as the "3 Red lines" which developers must adhere to, and which has meant most developers are limit to % or 5% debt growth at best.

For now it remains unclear how far the contagion will spread, although if Beijing stubbornly refuses to intervene, expect much more pain as capital markets seek to force Beijing's hand by make it unpalatable for the CCP to suffer even more selling which could spark social unrest.

"The price action across several asset classes in Asia today is horrendous due to rising fears over Evergrande and a few other issues, but it could be an overreaction due to all of the market closures," said Brian Quartarolo, portfolio manager at Pilgrim Partners Asia.

As discussed earlier, Xi faces a tricky balancing act as he tries to reduce property-sector leverage and make housing more affordable without doing too much short-term damage to the financial system and economy. Mounting concerns that he'll miscalculate are spreading ever-further beyond China-focused property developers and their suppliers.

"It's what the Chinese would describe as trying to get off a tiger," said United First Partners research Justin Tang, best summarizing Beijing's lose-lose dilemma.

Commenti

Posta un commento