Boom in Dodgy Wall Street Deals Points to Market Trouble Ahead

People 'going to get burned,' says Wall Street veteran Front

The fourth-quarter stock market rout that wiped out $12 trillion in shareholder value and sparked a bout of Christmas Eve panic may have quickly been forgotten by most Americans, but not by the salespeople and financial engineers of Wall Street.

No, the selloff, it would appear, wound up triggering fears that time was running out on the longest bull market in history. And so, when early 2019 delivered a miraculous rebound, they wasted no time in peddling all sorts of deals and arrangements that test the limits of risk tolerance: from health-food makers fast-tracked into public hands to stretched retailers wrung for billions by private equity owners in the debt market.

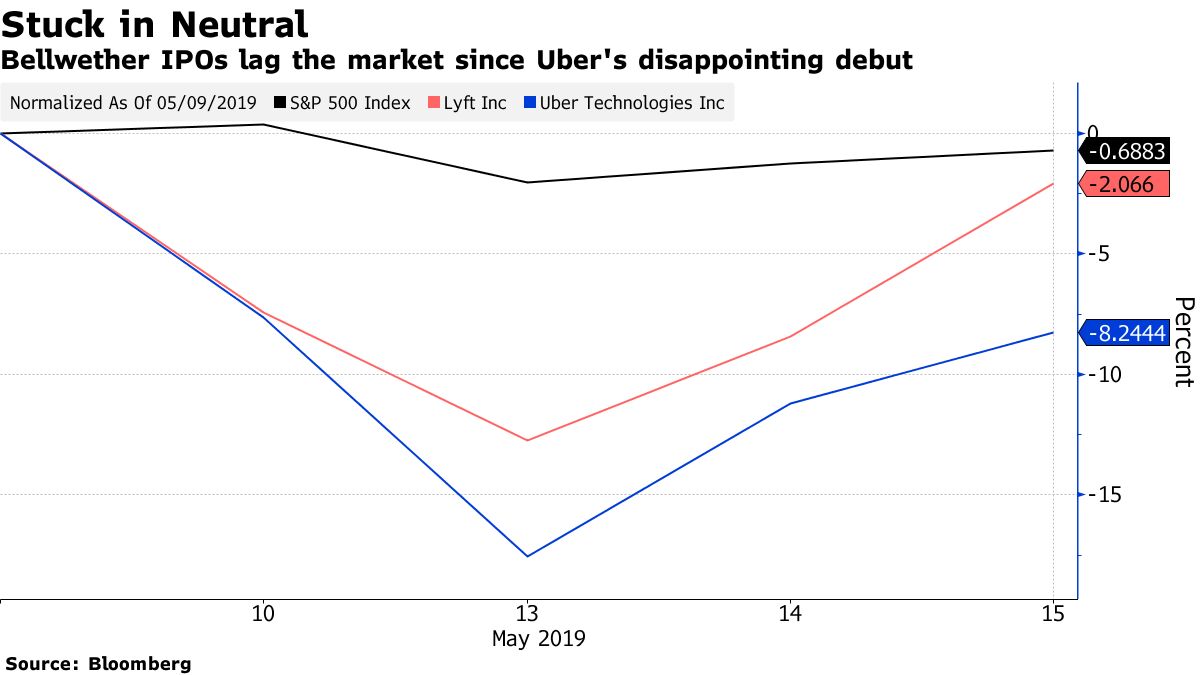

Junk bonds are flying out the door once again. Deeply indebted companies are borrowing even more to pay equity holders. And while you can't say the megadeal IPOs got rushed to market, two that were held up as heralding a return to IPO glory days have been flops. It's quickly turning Uber and Lyft into poster children for Wall Street eagerness amid an equity-market bounce that has all but banished memories of the worst fourth quarter in a decade.

"At some point, people are going to get burned," said Marshall Front, the chief investment officer at Front Barnett Associates and 56-year Wall Street veteran. "People want to take their companies public because they don't know what the next years hold, and there are people who think we're close to the end of the cycle. If you're an investment banker, what do you do? You keep dancing until the music stops."

Bankers who in October suggested a $120 billion valuation for Uber Technologies Inc. have eaten their words, with the market cap falling to half that. Rival Lyft Inc. closed its first day in March with a $25 billion valuation that was higher than all but about 275 U.S. companies. It's since fallen by a third. The timing of the IPOs only serves to further stoke the suspicions of those Wall Street observers who see a plot to transfer a private-market bubble into public hands.

JPMorgan, which ran Lyft's debut, declined to comment, while Morgan Stanley, lead underwriter for Uber, didn't respond to telephone and emailed requests for comment.

After 2018's traumas, credit markets have also reversed much of the carnage and rallied, giving license for companies to pick up the pace of borrowing. Junk bond issuance is now ahead of last year's pace, according to data compiled by Bloomberg. Last week alone saw $12 billion priced, the busiest in 20 months. Investment-grade issuance, though down from a year ago, is gaining steam, with back-to-back jumbo offerings this month from Bristol-Myers Squibb Co. and International Business Machines Corp., each around $20 billion.

Private equity firms have also taken advantage of benign credit conditions to cut risk and realize gains sooner. They've saddled the companies they invest in with more debt to pay themselves dividends. Issuance of leveraged loans for distributions to equity holders reached the highest in six months in April, according to data compiled by Bloomberg.

Sycamore Partners, a private equity firm know for aggressive bets in the retail sector, pulled a staggering $1 billion out of Staples Inc. last month through a recapitalization that increased the company's interest expense by $130 million annually. A few weeks later, Hellman & Friedman and Carlyle sold one of the riskiest types of junk bonds from drug research company Pharmaceutical Product Development LLC to help pay for a $1.1 billion dividend. The bond, which allows the company to delay interest payments, was the largest of its kind since 2017.

Concessions Lacking

Only in a few instances have investors extracted concessions from borrowers. Banks that financed the buyout of NSO Group -- an Israeli spyware company accused of selling software to governments and agencies linked to human rights abuses -- were forced to offer the debt at a steep discount to get it off their books, while Carlyle-backed ION Group this month dropped a planned $250 million dividend from a $2.2 billion leveraged loan sale, before ultimately opting to withdraw the entire debt deal.

Late-cycle behavior emerged in the bond market when state oil giant Saudi Aramco borrowed $12 billion in an unprecedented sale, staging a massive comeback from a year ago when Wall Street shunned the Kingdom in the aftermath of the assassination of journalist Jamal Khashoggi. But the bonds faltered in early trading, calling into question banks' claims that investors had put in an astounding $100 billion worth of orders to buy the securities.

In equities, bankers entered 2019 itching to unclog a massive pipeline of IPO hopefuls. Fresh off the worst fourth quarter of the bull market, prospects seemed grim -- until the turnaround came. As of this week, 89 initial offerings raised $27.2 billion in the U.S., the fastest start since 2014. While the vast majority have done well in a soaring market-- Beyond Meat Inc., Zoom Video Communications Inc. and Pinterest Inc., to name a few -- Uber and Lyft evoke nightmares of other IPO flops, like Snap Inc. and Blue Apron Holdings Inc.

Read more: A short seller bets it all on a spectacular market crash

In more modest districts of the new listing market, there's been hints of exuberance. The government shutdown that ended in late January created a backlog of filings for regulators. Banks turned to unusual tactics to keep the deal spigot flowing. Without a regulator around to review filings, these IPOs skipped the ordinary process of price discovery and instead took the risky step of disclosing a fixed IPO price 20 days before the stock began trading.

Seven companies set terms for IPOs while regulator offices were shuttered due to the federal government closure. A majority of them fell below their listing prices shortly thereafter. Included in this group is New Fortress Energy LLC, whose shares are trading well below the fixed IPO price used to push the deal through. Another IPO to launch during the shutdown, Guardion Health Sciences Inc., is now trading more than 60% lower than its fixed offering price.

Despite the best efforts of underwriters, not everything went through. The largest IPO attempted in the wake of the shutdown, Virgin Trains USA LLC, was withdrawn the same day it was expected to debut. Bankers spent nearly two weeks asking investors to value the firm as high as $3.15 billion before pulling the sale amid a pricing revolt from the buy side.

"People see it like this: it's been great until now, but the window is going to shut, the door is going to close, should we do something now because the next few years are a question mark?" said Front, the chief investment officer. "Wall Street gets a lot of money between now and then and they'll be able to put medals on their chest and say 'Look how we did' until they didn't anymore."

— With assistance by Elena Popina, and Kelsey Butler

Commenti

Posta un commento