... when in a a statement published at 1515ET, precisely when the S&P ramp started, the New York Fed confirmed it would dramatically increase both its overnight and term liquidity provisions beginning tomorrow through November 14th.

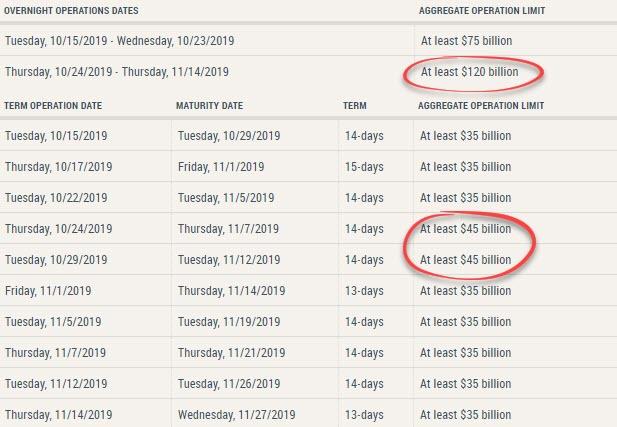

The Desk has released an update to the schedule of repurchase agreement (repo) operations for the current monthly period. Consistent with the most recent FOMC directive, to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation...

Amundi's Blanque Sees Excess Liquidity in Markets, Says Recession Risks Are Overdone

As we noted yesterday, that was a massive 60% increase in the overnight repo liquidity availability (from $75 billion to $120 billion) and a 28% jump in the term repo provision (from $35 billion to $45 billion).

"It's just more evidence the Fed will not back off as year-end gets closer," said Wells Fargo's rates strategist, Mike Schumacher. "The Fed wants to take out more insurance. You had repo pick up last week. That might not have gone over too well."

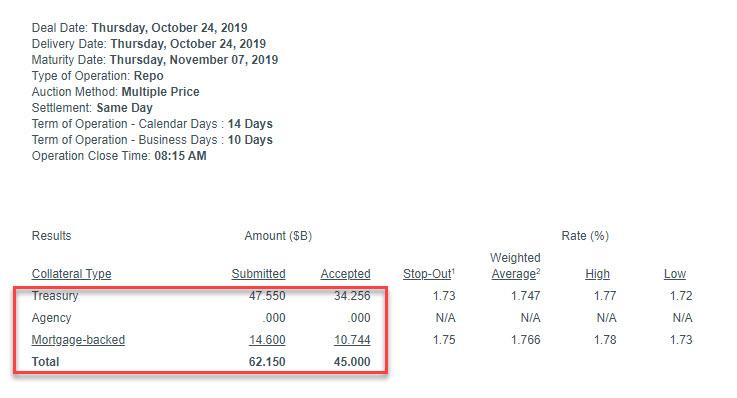

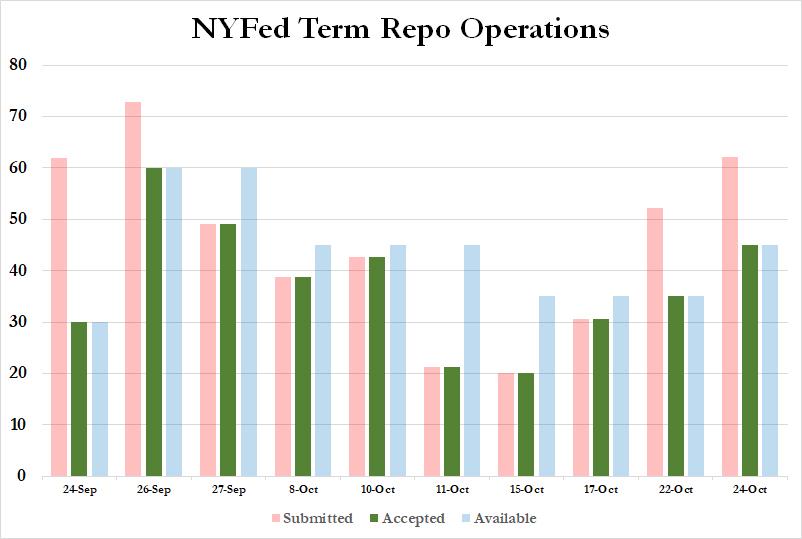

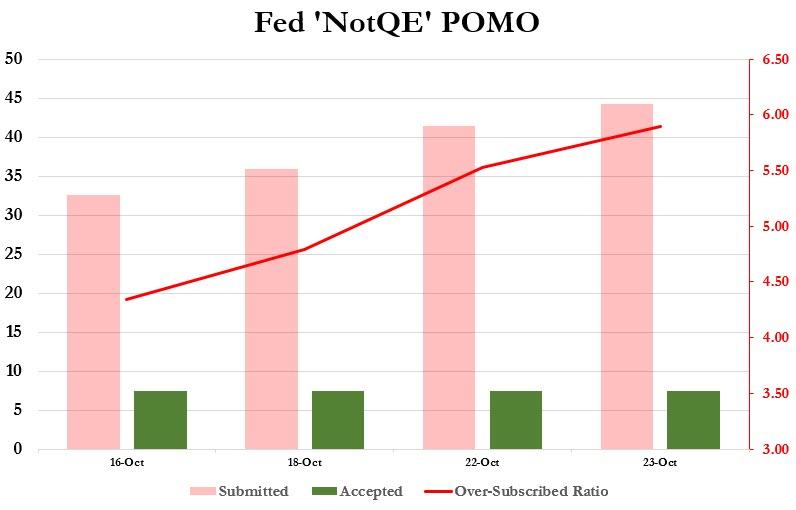

And now we know that there was good reason for that, because according to the latest, just concluded Term Repo operation, a whopping $62.15BN in securities were submitted to the Fed's 14-day operation, ($47.55BN in TSYs, $14.6BN in MBS), resulting in a 1.38x oversubscribed term operation, the second consecutive oversubscription following Tuesday's Term Repo, when $52.2BN in securities were submitted into the Fed's then-$35BN operation.

This was the highest uptake of the Fed's term repo operation since Sept 26.

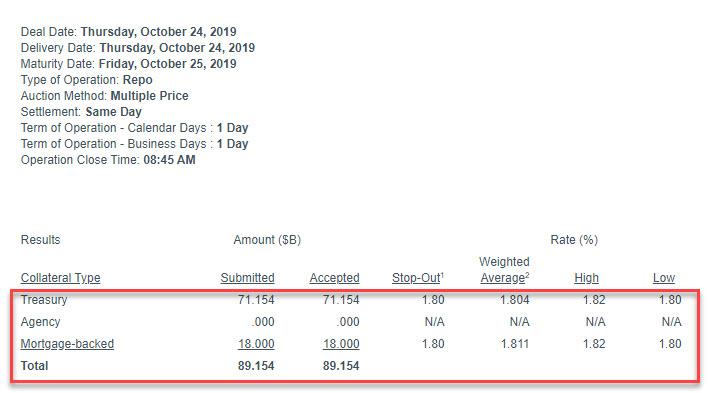

But wait there's more, because while the upsized term-repo saw the biggest (oversubscribed) uptake in one month, demand for the Fed's overnight repo also soared, with dealers submitting 89.2BN in securities for the newly upsized, $120BN operation.

This was the biggest overnight repo yet!

Meanwhile, funding tensions weren't evident only in repo, but also in the Fed's T-Bill POMO, where as we noted yesterday, demand for liquidity has also been increasing with every subsequent operation, peaking with yesterday's operation.

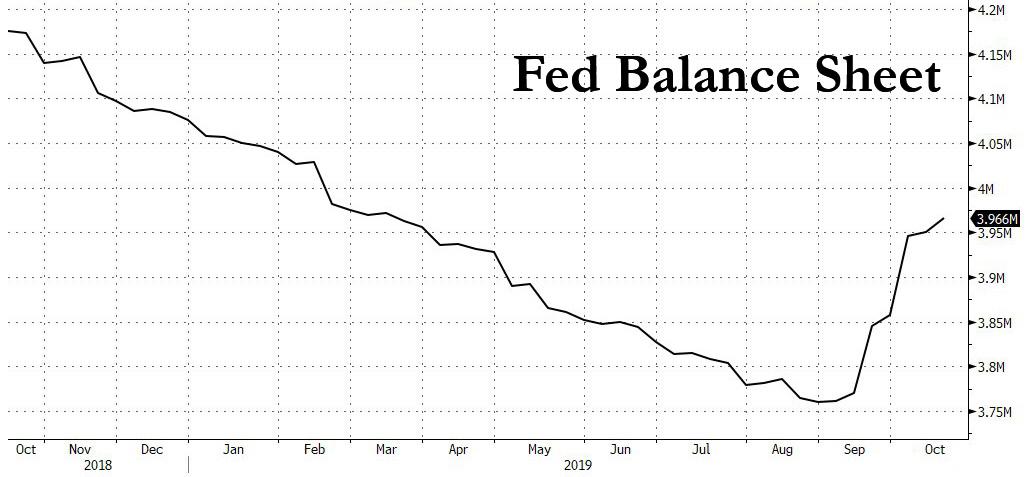

Needless to say, if the funding shortage was getting better, none of this would be happening; instead it appears that with every passing day the liquidity shortage is getting worse, even as the Fed's balance sheet is surging.

The only possible explanation, is someone really needed to lock in cash for month end (the maturity of the op is on Nov 7) which is when a "No Deal" Brexit may go live, and as a result one or more banks are bracing for the worst. The question, as before, remains why: just what is the source of this unprecedented spike in liquidity needs in a system which already has $1.5 trillion in excess reserves? And while we await the answer, expect stocks to close pleasantly in the green as dealers transform their newly granted liquidity into bets on risk assets.

Commenti

Posta un commento