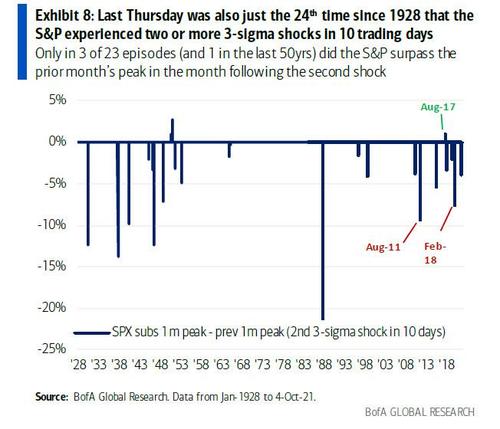

One week ago, Bank of America's derivatives team observed that "equity investors are losing confidence in Buy The Dip" and warned that after suffering a "meaningful setbacks in recent weeks," the coast appears far from clear. The bank pointed to recent episodes of increasing market fragility, and highlighted the recent market volatility manifesting in the second daily selloff of 3 standard deviations or more in just 7 trading days, only the 24th time since 1928 that the S&P experienced two or more 3-sigma shocks within 10 trading days.

Fast forward a week and BofA's increasingly bearish derivatives team led by Riddhi Prasad and Benjamin Bowler has intensified their warning, and pointing to the market's increasing trouble to rebound from its recent slump - it has now been 27 trading days without a record high, the longest such stretch since September 2020 - they note that momentum has been fading this fall, "and investor confidence in buying the dip may only keep waning the longer this sideways price action persists."

In the absence of proactive buyers - such as retail investors who have recently turned their back on the market, or aggressive stock buybacks which are currently in a blackout period due to the coming earnings season - the "market may for the first time since the Covid shock, need to test the Fed put in the next selloff," BofA warns.

Then, of course, we have the Fed's tapering. In an amusing interlude, BofA explains that the last time it warned that tapering is bearish, it got the usual "tapering is not tightening" platitudes from clients (spoiler alert: tapering is tightening as even Morgan Stanley now admits), adding that "the main pushback we received was that tapering asset purchases has a smaller economic impact than hiking rates, and is therefore a more minor threat than that of prior hiking cycles."

In response, the strategists counter that investors' should focus "not just on the way tapering and hiking change the underlying economics, but on their impact on investor sentiment in today's environment. For instance, just like the S&P thrived against 3 rate hikes in 2017 but choked on the 2018 hikes, a tapering cycle today could turn out as painful for the equity market as a prior hiking cycle."

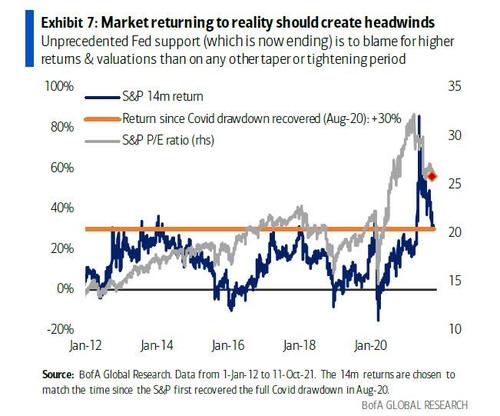

Elaborating on that point, BofA starts with the obvious, namely "that unparalleled monetary policy contributed to the historic returns and valuations achieved post-Covid."

But with tapering looming and lacking such explicit Fed support, and with momentum fading this fall, "the market may need a period of bad news to get the Fed back on its side or reach more attractive valuation levels. The longer the recent sideway action persists, the weaker the momentum and confidence that investors require to buy the dip."

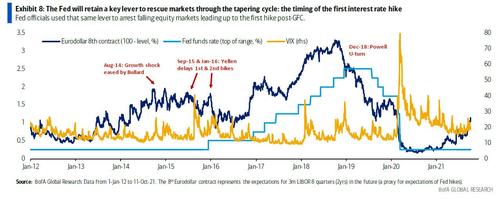

To be sure, the Fed will have one key lever to push stocks higher once tapering begins, namely jawboning about the timing of the first rate hike. That's the lever Fed famously used to reverse falling stocks leading up to the first hike post-GFC. In October 14, St. Louis Fed President Bullard stepped in to calm markets fearful of a growth shock. In 2015, on the back of another bout of stock market weakness, Yellen pushed back a largely-expected hike around the Sep FOMC meeting and then delayed the next hike for an entire year.

However, BofA cautions, "the option to delay hiking rates doesn't rule out a period of higher volatility", as:

- we still haven't seen how the market will react to the actual taper today,

- the change in Fed tune means the Fed put might have to be tested (vs. the dip getting bought in anticipation), and

- overshooting inflation might limit the Fed's ability to rescue the equity market as easily as it did during the last taper/tightening cycle (with inflation breakevens today well above anything experienced in the last taper and tightening cycles).

In a potential double-whammy, the fact that fixed income markets are not pushing back against the Fed's taper announcement lowers the Fed put strike, in BofA's view. That's because while traders generally tend to focus on equity market tantrums as the Fed's signal to intervene, major U-turns in Fed stance were often encouraged by the bond market 'disagreeing' with the Fed's plans.

For example, the 2013 taper tantrum was by far most felt in fixed income markets, while both inflation breakevens and expected rate hikes fell sharply as Powell raised rates through the second half of 2018, indicating that well ahead of the infamous Powell pivot they already knew he was on the right path.

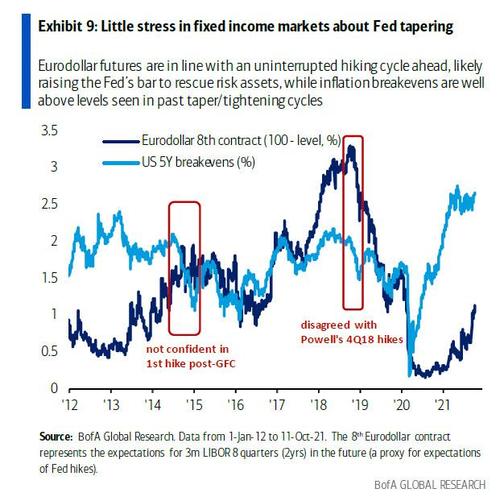

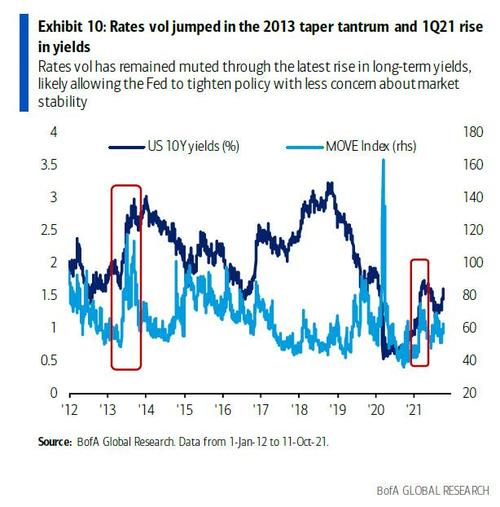

Today, on the contrary, Eurodollar futures implied rates and inflation breakevens are rising in line with an uninterrupted hiking cycle ahead (Exhibit 9) - perhaps because investors don't even bother to sell ahead of a market drop they know the Fed will step into and "rescue", while rates vol has remained muted through the latest rise in long-term yields (unlike in the short-lived Treasury selloff of 1Q21; Exhibit 10). This price action - driven by bonds - has raises the Fed's bar to easily change course if the equity weakness continues, and, as BofA warns, it calls into question where the Fed put strike is.

To summarize BofA's argument, between the coming taper and frequent recent warnings about euphoric markets from both FOMC talking heads and even the IMF today cautioning about a risk of sudden and steep declines in global equity prices and home values, the risk is the Fed put strike is (much) lower than the market anticipates, as:

- Equity valuations & returns have accelerated to extremes post-Covid,

- The bond market is projecting tightening is needed and

- Risks of inflation overshooting are increasingly real, with 5yr inflation break-evens well-above any level witnessed during the 2014-2018 taper/tightening cycle.

As a result, Prasad warns that "the Fed may be less willing to so easily deviate from tapering plans and talk the market back up as during the last cycle, further adding to risks." His conclusion - "bad news (delaying the Fed) would be the best news equities can wish for."

Translation: It's almost time for another crisis.

Commenti

Posta un commento