Over-the-Counter and Centrally Cleared Derivative Contracts at Banks in U.S. as of September 30, 2019 (Source: OCC)

After the epic financial crash on Wall Street in 2008 – the worst since the 1929 crash and ensuing Great Depression – two key reforms were put in place in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 to prevent another catastrophic meltdown on Wall Street.

The first key reform was that derivatives were to be moved out of the federally-insured, taxpayer backstopped commercial banks, that had been bought up by Wall Street trading houses, into units that could be wound down in a bankruptcy proceeding. It was called the "Push Out" rule. That reform was also meant to prevent the New York Fed from ever again secretly pumping upwards of $29 trillion into Wall Street trading houses and their derivative counterparties in order to bail out a corrupt casino banking system. (And yet here we are again today watching the New York Fed pump hundreds of billions of dollars each week into trading houses on Wall Street without offering any credible explanation to the American people as to why Wall Street is getting another bailout – and while mainstream media pretends this is as normal as apple pie by refusing to cover what's happening.)

Citigroup was able to get the Push Out rule repealed by having an amendment tacked on to a must-pass spending bill in December 2014.

The other promised reform was that derivatives would no longer be opaque private contracts (over-the-counter) between banks and insurers but would gain pricing transparency and adequate collateral backing by being traded on an exchange or centrally cleared at a clearing house.

But according to the most recent quarterly report from the Office of the Comptroller of the Currency (OCC), for the period ending September 30, 2019, an outrageous 81 percent of Goldman Sachs' derivatives remain over-the-counter. At JPMorgan Chase and Citibank, 53 percent of their derivatives remain over-the-counter black holes according to the OCC report. (See Graph 15 in the Appendix.)

We don't know how exactly how bad the situation is at Morgan Stanley because the OCC does not report the breakdown for its holding company, which has $36.2 trillion notional (face amount) in derivatives versus $903 billion in assets. We should note that Morgan Stanley owns two federally-insured banks while having the distinction of previously employing Howie Hubler, a bond trader who lost the bank $9 billion in bad bets during the last financial crisis. Morgan Stanley also has the distinction of receiving more than $2 trillion in secret cumulative loans from the New York Fed during the 2007 to 2010 financial crisis.

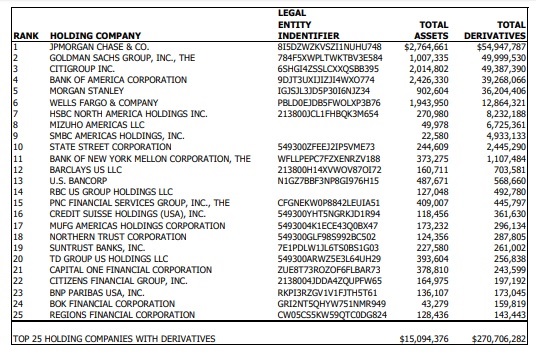

What the New York Fed knows that the majority of Americans do not know, is that five Wall Street investment banks – all of which own federally-insured, taxpayer-backstopped commercial banks – hold insane levels of highly-concentrated derivatives. There are more than 5,000 federally-insured, deposit-taking banks in the U.S. The vast majority of them see no reason to hold any derivatives as part of their banking business. But for reasons absolutely no one can explain, five Wall Street banks hold $230 trillion in derivatives, a stunning 85 percent of the $270.7 trillion in derivatives held by the top 25 bank holding companies in the U.S. (See OCC chart below.)

On June 30, 2010, a month before the passage of Dodd-Frank, Phil Angelides, the Chair of the Financial Crisis Inquiry Commission stated the following at a hearing convened specifically to examine "The Role of Derivatives in the Financial Crisis."

"I must say that despite 30 years in housing, finance, and investment — in both the public and private sectors — I had little appreciation of the tremendous leverage, risk, and speculation that was growing in the dark world of derivatives. Neither, apparently, did the captains of finance nor our leaders in Washington.

"The sheer size of the derivatives market is as stunning as its growth. The notional value of over the-counter derivatives grew from $88 trillion in 1999 to $684 trillion in 2008. That's more than ten times the size of the Gross Domestic Product of all nations. Credit derivatives grew from less than a trillion dollars at the beginning of this decade to a peak of $58 trillion in 2007. These derivatives multiplied throughout our financial markets, unseen and unregulated. As I've explored this world, I feel like I have walked into a bank, opened a door, and seen a casino as big as New York, New York. Unlike Claude Rains in Casablanca we should be 'shocked, shocked' that gambling is going on.

"As the financial crisis came to a head in the fall of 2008, no one knew what kind of derivative related liabilities the other guys had. Our free markets work when participants have good information. When clarity mattered most, Wall Street and Washington were flying blind…

"In June 2008, Goldman's derivative book had a stunning notional value of $53 trillion."

According to the September 30, 2019 report from the OCC, Goldman's derivatives book today is $49.9 trillion – an insignificant reduction of 6 percent in notional value after nine years of legislation, rulemaking and Congressional hearings.

The New York Fed is the primary regulator of the bank holding companies of Goldman Sachs, JPMorgan Chase, Citigroup (parent of Citibank), and Morgan Stanley. If these banks and their derivative exposures blow up the U.S. financial system and the U.S. economy for a second time, heads will roll at the New York Fed; its executives will be hauled before Congress; it will be stripped of its regulatory powers and money spigot to Wall Street; and those fat paychecks, drivers and limos will disappear. That's why the New York Fed is throwing hundreds of billions of dollars a week at a crisis it has yet to define.

Top 25 Bank Holding Companies in Derivatives as of September 30, 2019 (Notional Amounts, Millions of Dollars) Source: COC

Commenti

Posta un commento