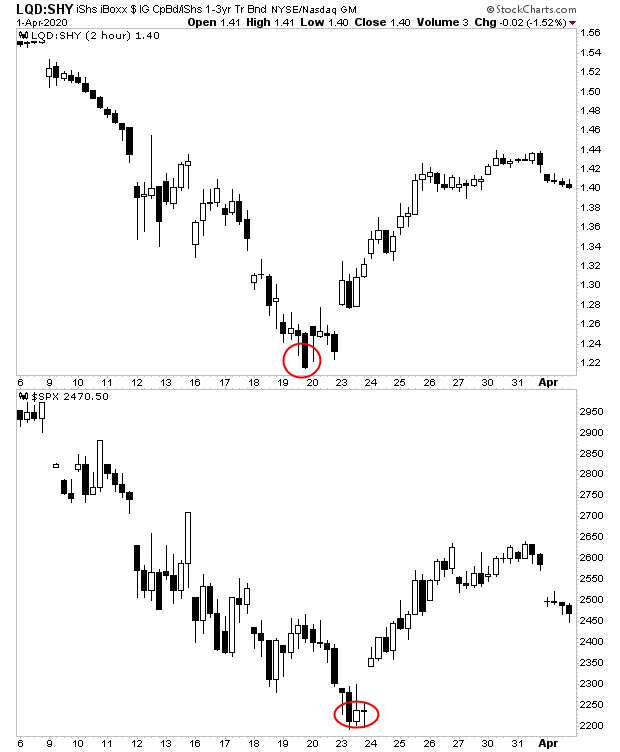

The Fed has announced it will buy investment grade corporate debt for the first time in history. The Fed also announced that it will be directly buying investment grade corporate debt ETFs like $LQD.

With that in mind, credit spreads on investment grade corporate debt have become "the canary in the coal mine" for this Fed intervention. If they collapse in a significant way despite the Fed buying them, then we know the Fed has failed to prop up the system.

You can see this in the below chart. Credit spreads for investment grade corporate debt actually bottomed on Thursday March 19th. Stocks didn't bottom until Monday of the following week.

Again, credit is leading stocks here. So if you want to get an idea of where the markets are heading you NEED to watch credit.

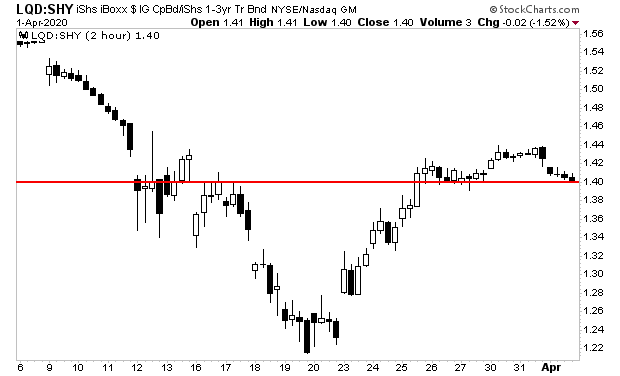

With that in mind, yesterday's breakdown was extremely dangerous for the credit markets. As you can see in the chart below, the drop brought credit right to THE line of CRITICAL support.

If we see a breakdown from here, then it's HIGHLY likely the system will go back into a panic and we will see new lows for stocks.

Commenti

Posta un commento