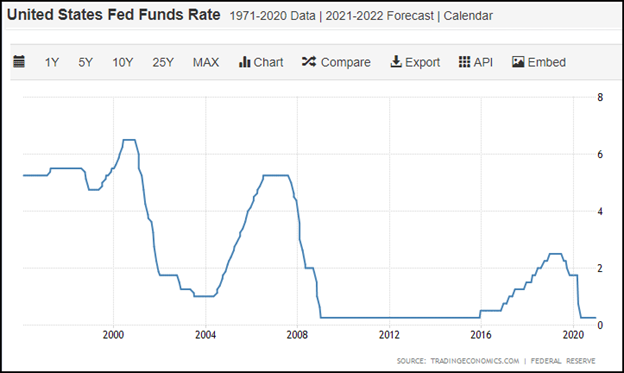

A look at the 5-year U.S. prime rate (the rate at which commercial entities borrow money) trend shows that interest rates are at multi-year lows. The country has not seen such low rates since the years following the financial crisis of 2008-09.

At 0.25% (twenty-five basis points), borrowing money is cheaper than it's been in a while – but not for everyone. And there's the irony: Banks, prosperous multinationals, and high net-worth individuals are the ones that really don't need "cheap money". Yet, that is the precise demography that benefit from ultra-low interest rates offered by banks, insurance companies and other corporate lenders.

So, where does that leave the struggling individual that just lost their job? Or, who do people in desperate need to pay off high-interest loans turn to? How can you make ends meet in the short term is you've got bad credit? The answer: You turn to the friendly short-term lender. But, while these providers of short-term financing – of up-to $1,000 and above – offer an vital service to their constituents, borrowing without considering the consequences may lead to further financial ruin.

Borrowing Made (too!) Easy

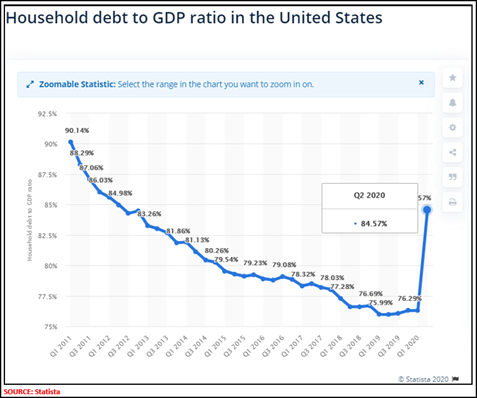

The quarterly (June 2020) U.S. household debt to GDP ratio currently sits at 84.57%. Putting that figure in perspective, it means that the average American owes 84.57 cents for every dollar that he/she earns. Doing the math, then, this means the average American only has a safety cushion of about 15.43 cents to tide them over in the event of an emergency – and that's not too much of a rainy-day fund!

So, when an emergency does strike, these Americans turn to easy-lending platforms online to make ends meet. The money is usually available within a day or two and, in most cases, the process is as simple as filling out an online form. Many lenders even have options that don't require a credit check. And that's great when people need money in a hurry.

The downside to easy lending platforms is that it makes borrowing extremely easy, and tempting – even for individuals who are already mired in debt. The simplicity of borrowing through such platforms, and the knowledge that the money is easily available whenever it's needed, causes many borrowers to disregard prudent debt management practices. It often ignites a spiral of unhealthy financial behavior:

- People spend beyond their means, and run-up high amounts of debt

- They'll borrow from a short-term lender or a payday loan shop to repay their creditors

- Then, when the payday/short-term loan comes due, they'll borrow some more to repay the initial loan

- They'll again use some of those loans to spend beyond their means

…and the cycle of financial recklessness repeats itself!

Sometimes, the deeper an individual gets into debt, the more attractive short-term borrowing solutions might appeal to their financial senses. And, with such financing available within as little as a few minutes, the instinctive reaction is to borrow now and consider the fall-out later. That's what borrowing made too easy does.

Understand the Financial Consequences

Since interest rates started moving downward, it has made access to loans less expensive. Individuals with significant credit card balances, or those owning mortgages or home equity loans, have seen interest payments declining over the last year or so. However, when it comes to short-term borrowing, those favorable rates are typically very elusive.

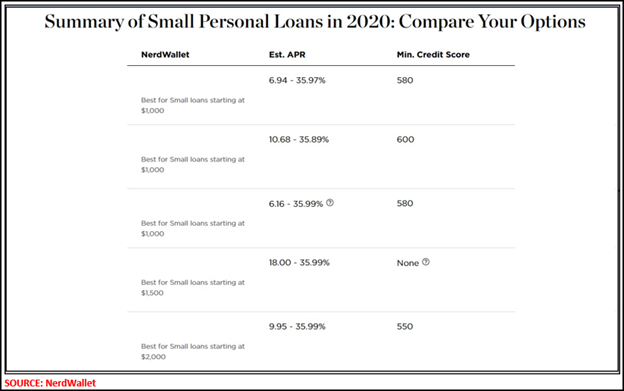

As indicated from a sampling of currently available short-term loans, one may expect an Annual Percentage Rate (APR) of nearly 36% for short-duration loans of $1,000 or more . Of course, you might look at the brighter side and think: Well, I might even qualify for the lower interest rate – 6.94% - but that might be an exception to the rule, and you'll need to:

- prove your credit-worthiness (past track record with the lender)

- have a steady employment history

- be earning significantly more than the $1,000 you intend to borrow

- (potentially) have a financially-sound individual vouch for you

And then, once you've received the money (typically within 24 to 48 hours – if all goes well), you'll still likely sit at a banquet of consequences with:

- higher (compared to many commercial banks or financial institutions) interest rates

- loan processing fees may be applicable

- late payment fees

- loan renewal charges and fees

By the time you put those added costs into the equation, your 36%, $1,000 loan may potentially cost you 38%, and you'll have paid over $217 in interest.

The important thing to understand is that, you can't just sign-on to a short-term lending portal and receive a loan. Even though there are lenders that offer credit to those with low, bad or no credit, there are consequences to recklessly taking on such debt.

Many short-term lending platforms offer quick, "no questions asked" loans. This often encourages many, who are in a financial crunch, to borrow for the short term, even before they crunch the numbers themselves, or understand the financial responsibility they are taking on. Some of those lenders go to great lengths to educate their clientele about the financial consequences of reckless borrowing. But when you're in a bind today, tomorrow's consequences often don't matter.

Choosing Your Lending Platform

We all find ourselves in a "financial pinch" at some time in our lives, and instinctively reach for a debt solution to tide us over. Unfortunately, some of us ignore the consequences of taking on debt to pay down debt!

The risk in doing that is that you could end up borrowing more than you can easily repay. Some short-term lenders are extremely careful to bring these financial traps to the knowledge of intending borrowers. They offer extensive financial education on their websites, so borrowers know what to expect even before they put in a loan application.

So, before you choose your lender for a cash advance, make sure you check out their reviews, blogs and other resources so you educate yourself on how short-term lending works. If you are knowledgeable about the risks, rewards and consequences attached to short-term borrowing, sometimes, turning to online lenders might be just the lifesaver some of us need!

Commenti

Posta un commento