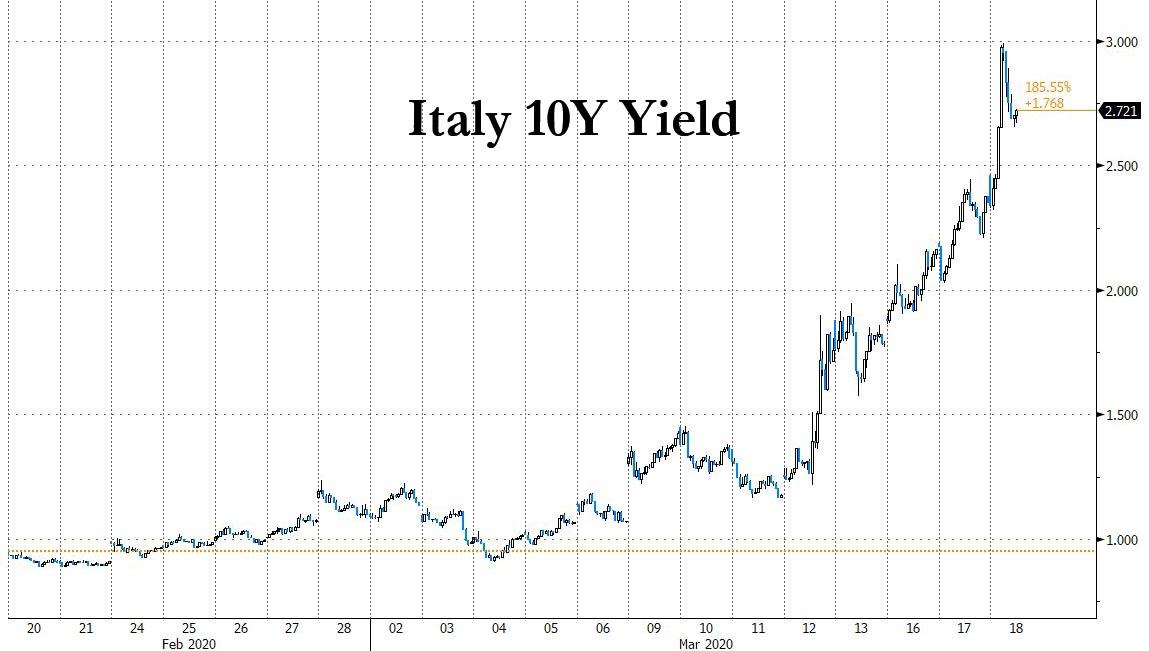

Then shortly after 6am ET, Italian bonds trimmed declines after Radiocor reported the ECB was invervening in the domestic market through the Bank of Italy. "Moves are flexible in terms of timing and of markets targeted, and can continue as long as needed", Radiocor news agency reported, citing central banking sources.

Even that, however, barely made a dent, with Italy's 10-year yield still almost 40bps higher at 2.72% after earlier climbing to 2.99%.

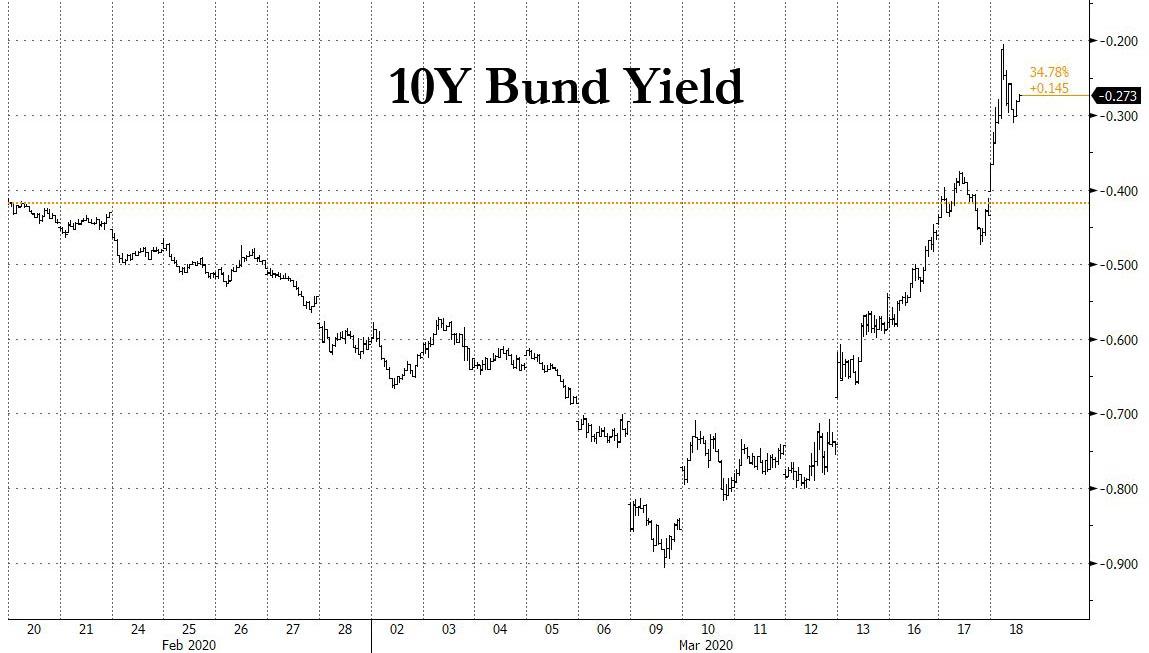

There was no ECB intervention in other European bonds, although they certainly also need it, with Bunds suffering sharp losses as the 10Y Bund yield surged as high as -0.20%...

... although paring some losses following reports Germany was softening opposition to Italy's proposal for joint EU bond issuance: German's 30-year swap spread narrows 11bps to 0bps, the tightest since 2014, amid concerns that any fiscal loosening will lead to more bond issuance.

The most notable however may be in 30Y Bund yields, which emerged back in positive territory, trading at 0.04% this morning, up from -0.5% less than a week ago.

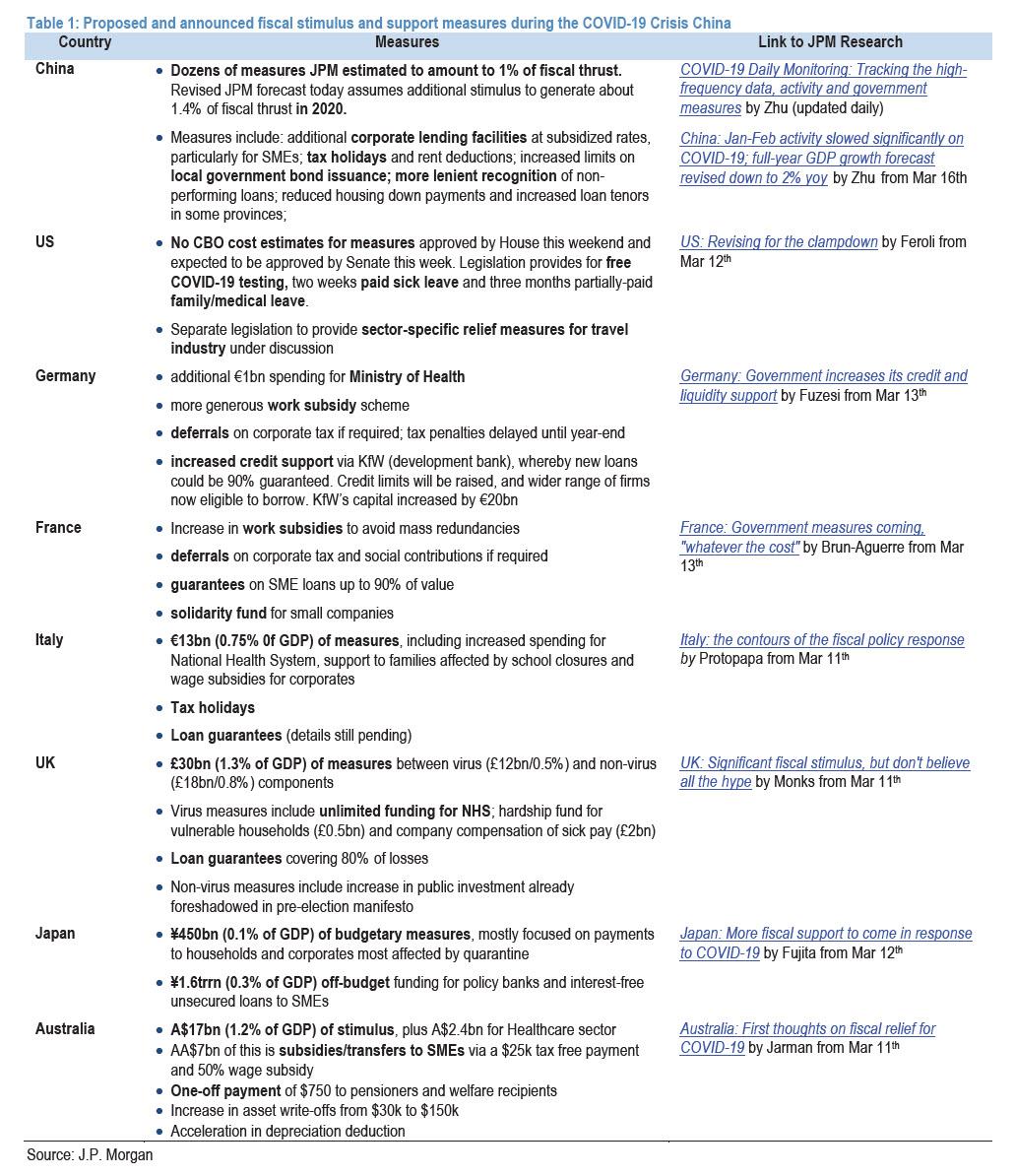

How soon until Lagarde wave a white flag and demands that the Fiscal stimulus tsunami which we summarized here last night...

... be immediately halted as the ECB simply does not have a large enough trading floor to buy everything that is suddenly breaking courtesy of helicopter money?

Commenti

Posta un commento